Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The UK property sector has a proud tradition of being the gloomiest corner of the European market in every crash. Not this time.

Global real estate, squeezed by rising interest rates, is in the midst of the worst slump since the financial crisis. Office occupancy and valuations have plummeted, especially in the US. Europe is faring better, helped in part by more accommodating lenders. But it is the UK that offers hope of a softer landing — testament to hard-learned lessons of the past.

Property groups used the free money era for debt-funded growth that has quickly become unsustainable at higher rates. It is no coincidence that the worst of the turmoil comes where the greatest excesses were seen in recent years. In Germany, say, where residential landlord Vonovia paid €18bn for rival Deutsche Wohnen. Or in Sweden, where SBB pursued an aggressive roll-up of health and education property. Both are selling assets fast to fix overstretched balance sheets.

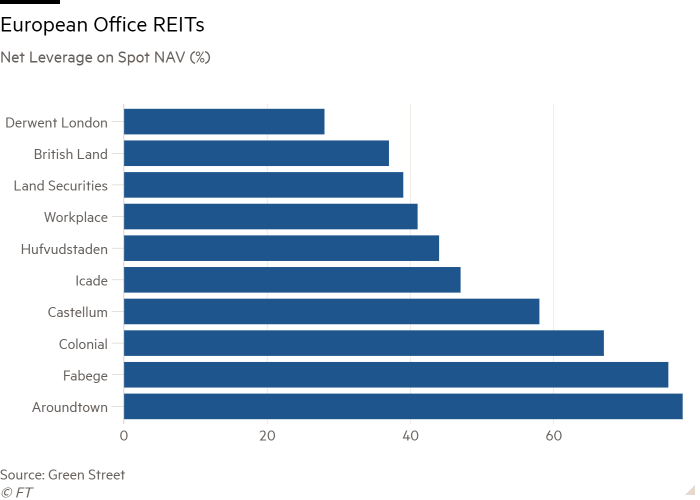

The UK’s biggest landlords, British Land and Land Securities, were in a similar position after the financial crisis. A more conservative approach to leverage since is helping to contain the damage in this downturn. Loan-to-value ratios for the two today hover in the mid-30s compared with almost 60 per cent in March 2009.

Continental office owners such as Fabege and Colonial both have LTVs closer to 40 per cent. Aroundtown, which invests in German offices, has an LTV close to 60 per cent.

Even the UK industrial and logistics sector, one of the frothiest areas of recent years, has also managed to keep leverage levels contained. Consolidation is under way. But deals such as LondonMetric’s offer for LXi Reit or Tritax Big Box move on UKCM are using shares (rather than cash) to preserve balance sheets. Post combination, loan-to-value ratios will be about 30 per cent for both.

Rental growth in European residential and industrial sectors has remained pretty strong. But falling office values have generally been exacerbated by a rental slump as tenants shun older, lower quality office buildings.

The UK market tends to be quicker to write down valuations, meaning a quicker adjustment to the new normal. British Land and Landsec cut portfolio valuations by 25 per cent and 15 per cent respectively in 2023, compared with 10 per cent for Aroundtown and Fabege.

The UK’s boom and bust sector went into this downturn hampered by the drag of Brexit. But it looks set to come out of it in relatively rude health.