Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

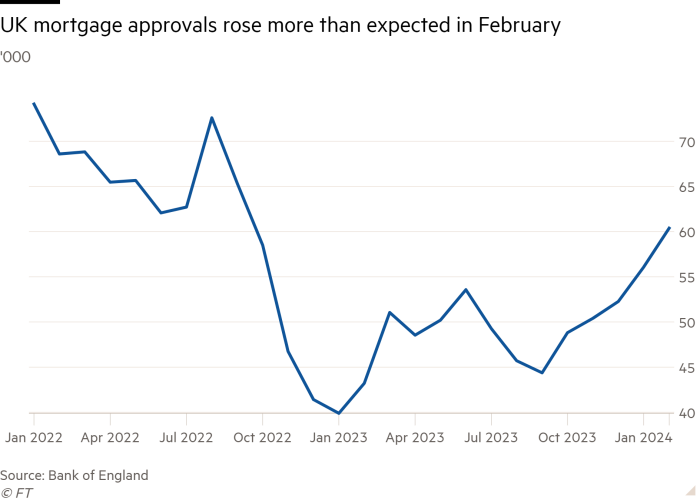

UK mortgage approvals beat expectations in February to hit their highest in 17 months, according to official data that reflects the fall in borrowing costs since the middle of last year.

Net mortgage approvals for house purchases rose to 60,400 in February from 56,100 in January, the Bank of England said on Tuesday. The figure exceeded the 56,500 forecast by economists in a Reuters poll and was the highest since September 2022.

The “effective” interest rate — the actual interest rate paid — on newly drawn mortgages fell 0.29 percentage points to 4.9 per cent in February, according to the central bank. It was the lowest rate since August 2023.

Separate figures published by lender Nationwide on Tuesday showed house prices unexpectedly dipped 0.2 per cent month on month in March.

But they were 1.6 per cent higher than in March last year, the fastest annual rate of increase since December 2022, and London remained the most expensive part of the UK.

Mortgage approvals and house prices are closely monitored by interest rate-setters as timely indicators of the health of the property market, which affects the wider economy and is important for monetary policy decisions.

The figures on Tuesday suggest the recovery in the housing market is continuing on the back of mortgage rates declining from their peaks in summer 2023.

The fall in most quoted fixed rates since the second half of last year reflects expectations that the Bank of England will this year cut interest rates from a current 16-year high of 5.25 per cent.

Some quoted mortgage rates have edged up since February because of sticky services inflation, a move reflected in the month-on-month drop registered by Nationwide in March. But analysts said the property market was on the mend.

Simon Gammon, managing partner at broker Knight Frank Finance, said: “The recovery in housing market activity is taking hold despite an uncertain start to the year for mortgage rates.”

“Hotter-than-expected inflation data in January and February prompted a few lenders to notch up mortgage rates, which knocked sentiment, but not enough to kill the market’s momentum,” he added.

The BoE data on Tuesday also showed other signs of the impact of higher interest rates fading, with cash deposits in household bank accounts rising in February driven by flows into instant access accounts.

“This provides further evidence that households are no longer searching for higher interest rates by tying up money in fixed-term accounts,” said Ashley Webb, economist at research company Capital Economics.

The figures from Nationwide — which put the average cost of a property at £261,142 — were worse than expected. Economists polled by Reuters had expected a month-on-month rise of 0.3 per cent in March, and an annual increase of 2.4 per cent.

The mortgage provider’s average house price was £12,600 below its August 2023 peak, reflecting the hit to prospective buyers from higher borrowing costs. But it was £45,200 more than in January 2020, before the pandemic, when the “race for space” and historically low interest rates drove up demand.

London was the most expensive region in the UK, with an average house price of £519,505. Prices rebounded in the capital in the first three months of 2024, rising at an annual rate of 1.6 per cent, up from a contraction of 2.3 per cent in the final quarter of 2023.

Northern Ireland was the best-performing region, with house prices rising by an annual rate of 4.6 per cent in the first three months of 2024, according to Nationwide. The north of England and Scotland also posted strong annual increases of 4.1 per cent and 3.7 per cent respectively.

The worst-performing areas were the south west of England and East Anglia, where house prices fell by 1.7 per cent and 1.3 per cent.