Anant Bhalla made a windfall transforming a regular life insurer into a successful play on private assets. In his next act, he wants to pull off a similar trick, but from the opposite vantage point.

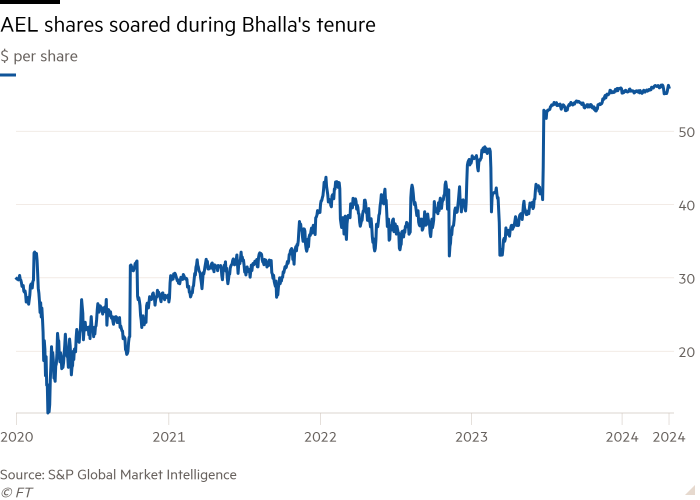

Bhalla is set to depart as chief executive of American Equity Investment Life when its $4bn sale to Brookfield Reinsurance closes in the coming days. The deal clinched him a $55mn bonus.

Bhalla is now seeking to raise $1bn in equity funding to build what he describes as a “merchant bank”. It will be part reinsurer, taking on $10bn to $15bn of long-dated insurance liabilities and investing a portion of the underlying funds in private credit and other alternative assets, and part investment manager and adviser to other insurance groups.

His wager is that he can earn higher returns, benefiting policyholders as well as insurers, an approach he says Warren Buffett’s Berkshire Hathaway pioneered.

“Traditional insurers are like frogs getting boiled in water,” Bhalla told the Financial Times. He said the old model, where they earned 1.5 per cent above returns promised to policyholders largely by buying low-risk bonds, was insufficient to cover their cost of capital and that 2 to 3 per cent would now be required.

“They need a solution on how to become alternative managers themselves.”

Bhalla is launching at a time when established private equity firms are busy building integrated insurance and private credit arms. Yet, at the same time, policymakers around the world are ringing alarm bells about this nascent business model.

The attraction is that the insurance premiums provide a cheap source of long-term, stable capital to lend out in the fast-growing and lucrative private credit market, which already has reached $1.7tn in assets.

Meanwhile, organisations such as the National Association of Insurance Commissioners (NAIC) and the IMF have raised warning flags about hard-headed financial investors mixing themselves up in the retirement funds of millions of future pensioners.

Bhalla was a longtime insurance executive with previous stints at AIG and MetLife when he arrived at AEL in 2020. The Iowa-based company is among the largest sellers of retirement annuities, a status that made it the target of a hostile bid made jointly by Apollo Global Management and MassMutual not long after Bhalla took charge.

AEL rejected the overtures and launched a strategic plan Bhalla would call “AEL 2.0”. The company eventually put a quarter of its customer premiums into various private asset classes including middle market corporate loans and vehicles that bought single-family homes.

In some instances it bought equity stakes in asset managers, including 26North, a firm launched by Apollo co-founder Josh Harris, and which had a multibillion dollar reinsurance agreement with AEL.

Bhalla maintains that private asset investing earns higher returns in exchange for illiquidity — rather than greater credit risk — and that this illiquidity is less problematic because benefits owed to policyholders are not due for several years. Shareholders in the insurer also benefit from the higher returns.

His new venture will be a “merchant banking model for insurance”, Bhalla said. In addition to taking on life insurance premiums through reinsurance agreements with primary insurers, it plans to offer outsourced investment management to insurers looking for expertise in private assets, and to syndicate some of its investments to third-parties.

It will also differentiate itself as a “thematic” investor. Bhalla cited data centres and cold storage as areas that needed capital to expand and which have decades-long investment horizons.

He believes that the biggest private capital businesses are at the stage of having to grow for the sake of it or to maximise management fees. “Our objective is not to build another firm that exists just to feed the beast,” he said.

BlackRock chief executive Larry Fink wrote in his annual shareholder letter in March that new investment strategies would be required to meet the financial needs of a global population that is living longer but has under-saved for retirement.

But regulators worry about excessive risk taking by newcomers with new business models.

The NAIC has raised concerns about the industry exposing insurance policyholders to risky investments such as collateralised loan obligations, which played a major role in the financial crisis.

The IMF said recently that private equity-backed insurers were “more vulnerable” to a credit downturn, due to their higher proportion of illiquid assets, and has previously warned about potential “contagion” seeping into the wider financial sector and economy.

There have also been a handful of recent industry blow-ups. A roll-up strategy launched by European private equity group Cinven ran into trouble after one of the life insurers it bought foundered because of a rush of withdrawals by annuity holders.

In the US, insurers that have taken on exposure to the private equity firm 777 Partners are under fire from regulators and rating agencies for potentially excessive risk-taking.

Bhalla acknowledged that these mis-steps had complicated life for others in the industry. But he insisted alternative investment strategies were crucial for the sector’s financial future. “Without private assets, insurance cannot work.”

In March, Japan’s Dai-ichi Life Holdings took a stake in Canyon Capital, a $20bn credit manager that made its name as a distressed and opportunistic debt expert. Within a few years, Dai-ichi will have the chance to buy all of Canyon.

In April, Blue Owl Capital spent $750mn buying Kuvare Asset Management, a decade-old asset manager dedicated to insurance, which resembles Bhalla’s venture.

One industry veteran noted that banks withdrawing from business lending in response to tougher capital rules since the financial crisis was a central factor in the convergence of private assets and insurance.

Don Mullen, the founder of Pretium, a private capital manager that Bhalla partnered with at AEL, said that insurers are increasingly the venue of choice for corporate lending.

“The fact remains that bank balance sheets are not attractive for illiquid assets that have above average volatility,” Mullen said.