Five-year fixed mortgage rate hits 6%

UK borrowers continue to be hit by higher mortgage rates as the cost of living squeeze continues.

The average five-year fixed residential mortgage rate has hit 6.01% today, up from 5.97% on Monday, data from the financial data provider Moneyfacts shows.

That’s the highest level since last November, when mortgage rates had been driven up by the mini-budget chaos last autumn.

Shorter-term mortgage rates also continue to climb. The average two-year fixed residential mortgage rate has jumped to 6.47, up from 6.42% on Monday.

The average two-year fixed was last higher on 31 October 2022 (when it was 6.48%).

These fixed-term rates have climbed in recent weeks as the UK’s persistently high inflation rate has pushed up interest rate expectations.

Two-year government bond yields, which are used to price fixed-rate mortgages, yesterday hit a 15-year high of 5.3%.

Analysts have warned that more than a quarter of UK homeowners on a fixed-rate mortgage face sharp increase in monthly payments before the next election.

Economists at the Resolution Foundation thinktank predicted last month that total annual home loan payments were on course to rise by £15.8bn by 2026 – delivering a £2,900 blow for the average household remortgaging next year.

Key events

Ineos owner Jim Ratcliffe accuses UK regulator of being ‘hostile to business’

Sir Jim Ratcliffe, the owner of chemicals giant Ineos, has accused Britain’s competition regulator of becoming “increasingly hostile to business”.

Ratcliffe took a break from his pursuit of Manchester United to criticise the Competition and Markets Authority for blocking Ineos’s purchase of a concrete additives business being sold by Swiss chemicals group Sika earlier this year.

Ratcliffe, the FT reports, said the CMA’s decision was “yet another example of a deal being stopped that would benefit the UK”.

Ratcliffe accused the CMA of “building a reputation as an overly aggressive regulator with little regard for the impact of its decisions on UK business”.

He also said:

“Add to this, the ridiculous North Sea windfall tax and continuing high energy costs and we are seeing a government that is driving business out of the UK.”

The CMA was also criticised by Microsoft and Activision Blizzard for blocking their merger earlier this year.

The regulator, though, has insisted that “effective merger control is pro-business and pro-growth.”

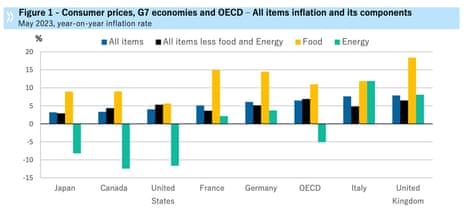

UK only G7 country with rising inflation, says OECD

The UK is experiencing a sharper inflationary squeeze than other advanced economies, a report from the Organisation for Economic Co-operation and Development shows.

The OECD reports that the UK is the only member of the G7 where inflation rose in May.

Year-on-year inflation in the G7 fell to 4.6% in May 2023, from 5.4% in April, the OECD reports, which is the lowest level since September 2021.

It says:

Inflation declined in all G7 countries apart from the United Kingdom, where inflation edged up, as core inflation continued to rise.

The lowest inflation rates among G7 countries were registered in Japan and Canada, both below 3.5%.

In the UK, the Consumer Prices Index including owner-occupiers’ housing costs (CPIH) rose by 7.9% in the 12 months to May, up from 7.8% in April.

But headline CPI (which is tracked by the Bank of England) was flat at 8.7% in the year to May.

The OECD adds:

Food and energy inflation remained the main contributors to headline inflation in Italy, while core inflation was the main inflation driver in France, Germany, Japan, the United Kingdom and the United States.

The government minister Johnny Mercer has suggested banks could be “profiteering” by failing to pass on interest rate increases to savers, while continuing to hike mortgage rates.

Mercer told Sky News:

Interest rates are going up and the government wants to see those passed on to savers.

You don’t want to see any profiteering like this, particularly when life is really tough for people out there at the moment around interest rates.

Today’s Moneyfacts data showed a four percentage point difference between the average two-year fixed mortgage (6.47%), and the average easy access savings rate (2.45%).

Full story: Average rate on five-year fixed mortgage deal in UK climbs above 6%

Zoe Wood

A typical five-year fixed mortgage deal in the UK now has an interest rate of more than 6%, putting further pressure on borrowers who are hoping to buy a home or reaching the end of their existing deals.

Data from the financial information firm Moneyfacts shows the cost of a five-year deal for homeowners rose to 6.01% on Tuesday, up from 5.97% on Monday. It is the highest level since last November, after mortgage rates had been driven up by the mini-budget chaos of last autumn.

The average two-year fixed deal is now 6.47%, up from 6.42% on Monday.

Mortgage lenders have been increasing rates and withdrawing deals after the Bank of England raised interest rates by half a point to 5% last month in an attempt to curb high inflation.

Threadneedle Street has now raised interest rates 13 times since December 2021. But inflation – which measures the rate at which prices are rising – remained stubbornly high at 8.7% in May. The UK’s official inflation target is 2%.

The rapid rise in the base rate is bad news for millions of borrowers whose home loan deals are due to end in the coming weeks and months, as many currently enjoy a rate of less than 2%. The prospect of a huge jump in mortgage payments comes as Britons struggle to cope with higher food and energy bills.

More here:

Jeremy Hunt has urged UK banks to pass on higher interest rates to savers.

The chancellor says the FCA has his “full backing” ahead of the regulator’s meeting with banks to examine the gap between spiralling mortgage costs and savings rates.

Increased interest rates must also be passed on to savers.@TheFCA has my full backing to ensure banks are passing on better rates as they should be. https://t.co/7JSWyEWewA

— Jeremy Hunt (@Jeremy_Hunt) July 4, 2023

The latest uptick in mortgage rates spells even more misery for borrowers, says Myron Jobson, a senior personal finance analyst at interactive investor:

It is a gut punch to the around 800,000 households with a fixed-rate mortgage deal set to expire in the second half of this year. Higher mortgage rates means borrowers end up shelling out more in interest over the life of their loans. This translates into higher monthly mortgage payments which would weigh heavily on homeowners already struggling to battle the inflationary beast in other areas of expenditure like food bills.

Many borrowers will be desperately rubbing their figurative crystal ball to get an idea of where mortgage rates are heading in the not too distant future. When interest rates are on the rise, deciding between a short- or long-term fixed-rate mortgage deal requires careful consideration. Ultimately the decision between a short- or long-term fixed-rate mortgage depends on your individual circumstances. It is worth consulting a mortgage adviser to explore your options.

Nationwide building society reported last Friday that house prices had fallen by 3.5% in the last 12 months.

This “recalibration” in house prices is the only positive outcome of higher rates for buyers, Jobson adds:

The latest increase in mortgage rates threatens to shatter the resilience in house prices in June observed in Nationwide’s latest house price index.

But the combination of higher mortgage rates and already inflated home prices has significantly limited what wannabe homeowners can afford, pushing many of them out of the market. This has a ripple effects on the rental market. With fewer home sales, more people will continue to rent, potentially causing rent costs to go up.

Sandra Laville

Water companies must pay to fix illegal sewage discharges rather than pass the cost to customers, lawyers for the charity WildFish are to argue in the high court today.

The campaign group will allege at a judicial review that the government’s £56bn plan to reduce raw sewage dumping from storm overflows is illegal. More details here …

Thames Water fined £3.3m for ‘reckless’ sewage discharge

Thames Water has been fined £3.3m for a “reckless” incident in which “millions of litres” of undiluted sewage was pumped into rivers near Gatwick airport in 2017.

A two-day sentencing hearing at Lewes crown court was told there was a “significant and lengthy” period of polluting the Gatwick stream and River Mole between Crawley in West Sussex and Horley in Surrey on 11 October 2017.

The judge Christine Laing KC said on Tuesday that said she believed Thames Water had shown a “deliberate attempt” to mislead the Environment Agency over the incident, such as by omitting water readings and submitting a report to the regulator denying responsibility.

Thames Water pleaded guilty on 28 February to four charges relating to illegally discharging waste in October 2017.

This penalty comes as the utility giant, which serves 15 million households across London and Thames Valley, faces concerns over its future amid mounting debt.

The record fine against a water company for illegal discharge of sewage is held by Southern Water at £90m for nearly 7,000 incidents across Hampshire, Kent and Sussex in a case brought by the Environment Agency in 2021.

Sainsbury’s CEO: Higher wages will fuel food inflation

Food prices in Britain will not return to where they were before Russia’s invasion of Ukraine, the boss of Sainsbury’s has warned.

Hours after announcing that food inflation was falling, Simon Roberts predicted that a permanent rise in labour costs will mitigate the easing of commodity and energy pressures.

Roberts has cautioned that food inflation will still be a challenge going forward as higher labour costs were now fixed into the operating models of food retailers and suppliers.

He said that while falls in commodity costs had driven recent price cuts in fresh food products, such as milk, butter, bread, pasta and rice, prices of packaged goods would be more stubborn.

Roberts told reporters:

“We should just remember that energy costs are still high and labour costs have been elevated permanently.

“So we would expect inflation to continue to improve, but it’s not going to go back to where it was before because the cost of producing food is clearly elevated from where it was a year or two back.

Basic pay is growing by 7.2% per year, according to the latest labour market data – the fastest rate on record, but still slower than CPI inflation which was 8.7% in April and May.

Paul Welch, the CEO of the London-based adviser LargeMortgageLoans.com, fears that mortgage rates will continue to rise until inflation is brought under control.

Welch says:

As long as swap rates, the rates which banks pay to borrow money, remain high, then fixed rates for mortgages will continue to rise.

If core inflation doesn’t come down significantly this month, or God forbid rises, then interest rates and swap rates will continue to go up and up. It gives me no pleasure to say that we could realistically see some fixed rates reach 7% before the summer is out.

Currently, 10- and 15-year swap rates are the best value for money, so if you like the stability of a fixed rate and you can afford to fix for the long term, then you could try a 10-year fixed rate mortgage, with a rate of less than 5% currently.

🇬🇧 UK Five-Year Mortgage Rate Breaches 6% for First Time This Year

The average five-year fixed-rate home loan rose to 6.01% on Tuesday, edging closer to the 14-year peak reached at the end of 2022.

The average two-year fixed-rate deal rose to 6.47% after breaching 6% for the… pic.twitter.com/0iMx9xvU9C

— PiQ (@PriapusIQ) July 4, 2023

The Liberal Democrats’ Treasury spokesperson, Sarah Olney, has urged the government to do more to help borrowers, after the average five-year fixed mortgage deal surpassed 6% this morning.

She said:

This is yet more mortgage misery for homeowners on the brink.

Rishi Sunak asking homeowners to hold their nerve is sounding more tin-eared by the day.

It shows this Conservative government is just totally out of touch.

Conservative ministers sent mortgages spiralling through all their chaos and incompetence; now they are refusing to lift a finger to help.

The Lib Dems are proposing a £3bn emergency mortgage protection fund to protect people whose homes would otherwise be repossessed due to rising interest rates.

The bakery and coffee chain Le Pain Quotidien has shut nine UK sites with the loss of 250 jobs after falling into administration.

BrunchCo UK, the company trading as the high street chain, has confirmed it hired administrators from Kroll.

Eight cafes in London and one in Oxford’s recently refurbished Westgate Centre have shut as a result of the insolvency.

The Le Pain Quotidien site at St Pancras railway station run by sister company SPQ Holdings Limited will continue to operate.