Receive free Markets updates

We’ll send you a myFT Daily Digest email rounding up the latest Markets news every morning.

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Yesterday we asked if anything was stopping the Fed from raising rates. At a central bankers’ conference on Wednesday, Jay Powell gave his answer: no, not really. “Although policy is restrictive, it may not be restrictive enough and it has not been restrictive for long enough,” the Fed chair said. Markets shrugged. Tell us what we should be writing about: robert.armstrong@ft.com and ethan.wu@ft.com.

A close look at office Reits

Yesterday we presented the Unhedged view of the US commercial real estate market, which is under pressure from higher interest rates and work from home. The summary is that stresses are rising, but they are mostly confined to a small slice of the market: low-quality properties. Vacancies and delinquencies are above pre-pandemic levels, but are not shooting higher. That said, the problems remain confined only because the economy (in the ways that matter) remains remarkably strong. In a proper slowdown or recession, the CRE dominoes could start to fall.

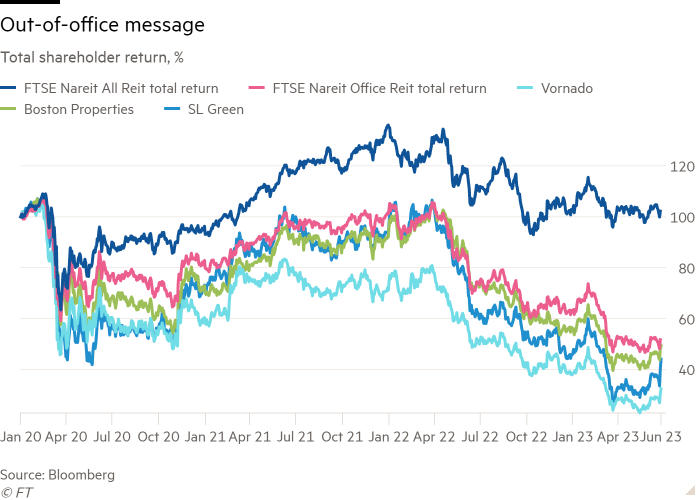

Is there an investment opportunity in there somewhere? One obvious place to look is office real estate investment trusts, the companies that own the category of commercial property that is performing the worst. Here’s a total returns chart of three of the biggest — Boston Properties, Vornado and SL Green — along with an office Reit index and an all-Reit index:

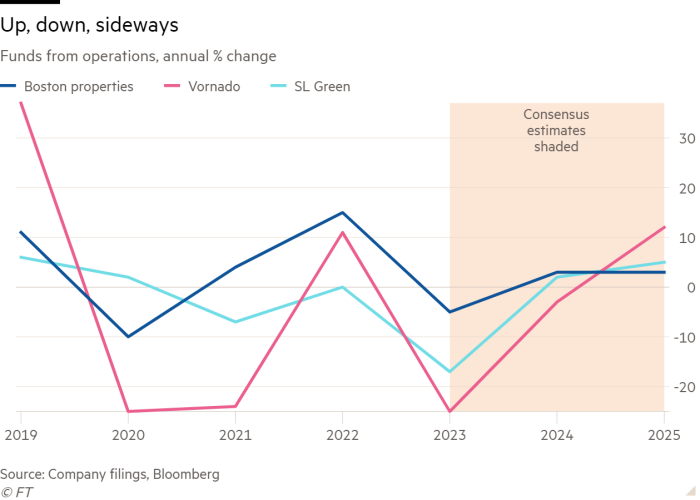

Even including dividends, the office Reits have lost half or more of their value since the start of the coronavirus pandemic. That’s a lot! One might say (to simplify significantly) that the market is making a collective bet that profits at these companies are going to drop by half. Are things really going to be that bad? Three years into the pandemic, and almost a year into the higher rates regime, the damage to earnings has not been so great. Here is a chart of annual changes in cash flows available for distribution at the three big office Reits:

Real estate companies’ cash flows are volatile, and 2019 was a very strong year for all three companies, making comparisons hard. But the basic picture here is that cash flows are flat to down, not driving off a cliff. In addition, Wall Street analysts’ consensus foresees stability for the next three years. Granted, you can probably discount those estimates somewhat: the stock prices are telling you that the investors’ consensus is that the analysts’ numbers have to come down. But as of now, disaster has not struck, and the companies are trading as cheaply, relative to their cash flows, as they have since the depths of the financial crisis. Boston, Vornado and SL Green trade at eight, seven and six times funds from operations, respectively. As recently as March 2022, those multiples were at 16, 13 and 11. Half off!

The basic buy case would have two parts. While it is clearly impossible to predict what vacancies and rents are going to look like when the work-from-home trend settles into a steady state, the valuation is giving you a wide margin for error on your best guess. And while the rate outlook is uncertain, it looks as if rates are near a peak now, and any decline from here would be a bonus.

The problem is that the two big risk factors — building revenue and interest rates — compound one another and could interact in various ways. Higher interest rates increase the financing costs on any building that is financed with floating-rate debt or has to roll over its debt. Lower occupancy or lower rent reduces building incomes. If both happen to the same building, that building could end up being owned by its lenders, triggering a distress sale — with further repercussions for other buildings in the market, and other real estate borrowers. The very low valuations of the office Reits reflect the fact that CRE is a highly leveraged and interconnected industry where, if things go wrong, quite unexpected and very bad things might happen.

The big Reits themselves have two basic stories to tell to reassure investors. One is that they have structured their debt prudently, which will carry them though the current storm. Here is Steven Roth, chief executive of Vornado, talking to analysts recently:

We rely primarily on project-level non-recourse debt, old-fashioned mortgages. Only 2.5 per cent of our debt is recourse and that with well-laddered maturities. We are clear eyed and realistic about the near-term financial market challenges. It is not pretty when 3 per cent debt rolls over to 6, 7 or even an 8 market. We will certainly have a few workouts [ie, debt renegotiations] to deal with over the next couple of years. But that is the point of having non-recourse debt. We have no maturities this year, limited property-level maturities next year and no corporate maturities in 2025 with sufficient capacity on our line that matures in December 27 and so that we don’t have to finance in the current hostile market.

“Non-recourse debt” means debt owed against the building, not by the company itself; the point is that a workout on one building needn’t imperil a Reit’s entire balance sheet.

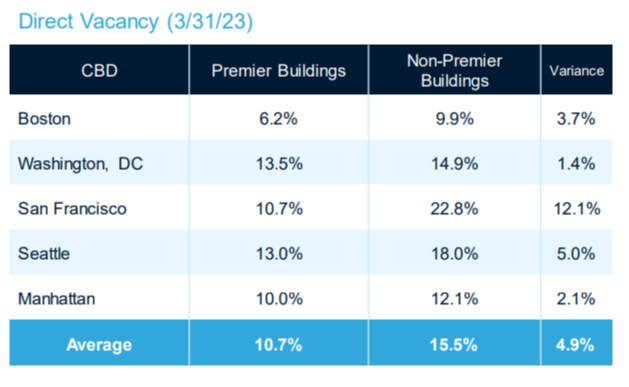

The second point of reassurance is that the bad problems should remain confined to the low end of the market, as they have so far, and the big public Reits specialise in high-end properties. Here is a Boston Properties slide from a recent presentation touting the lower vacancy rates of high-end buildings (the data comes from CBRE):

Anthony Paolone, real estate analyst at JPMorgan, sees some truth in the idea that high-end office properties will be spared the worst in this cycle. But he thinks the problems besetting the sector did not start with the pandemic. Demand for office space was already in slow decline as employers cut space per employee, and this has only been compounded by work from home. Meanwhile, both tech and financial services, which make up an important part of the high-end tenant base, are facing cyclical pressures. Rising rates top it all off. “If it was any one of these problems, the industry would work it out. But it’s all three at once.” He has underperform ratings on Boston, Vornado and SL Green.

For anyone who is sceptical of the work-from-home trend and thinks interest rates can fall without a hard landing or recession, office Reits offer a lot of upside. For Unhedged, it’s too many forms of interacting risk all at once.

One good read

We wrote last week that a US liquidity boom was fading. In the Financial Times, Michael Howell makes the opposite case.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.